Helix Octo Factor Model

A Proprietary Quantamental Framework for Idiosyncratic Alpha

The Octo-Factor Model: Pricing Forensic Integrity and Eco-Efficiency

The market chronically misprices the divergence between “Green Talk” and “Green Walk” and forensic decay, creating a structural alpha gap that narrative-driven ESG scores consistently fail to capture

.

If you are still using Fama-French or CAPM to price this market, you are pricing a ghost. Those models measure value but fail to measure the sustainability of that value, and they certainly ignore integrity. I have spent 25 years watching narratives destroy capital because investors refuse to audit the unit economics of the “next big thing.” Traditional models price risk, but they do not price the forensic decay that precedes a narrative collapse by 12 to 18 months.

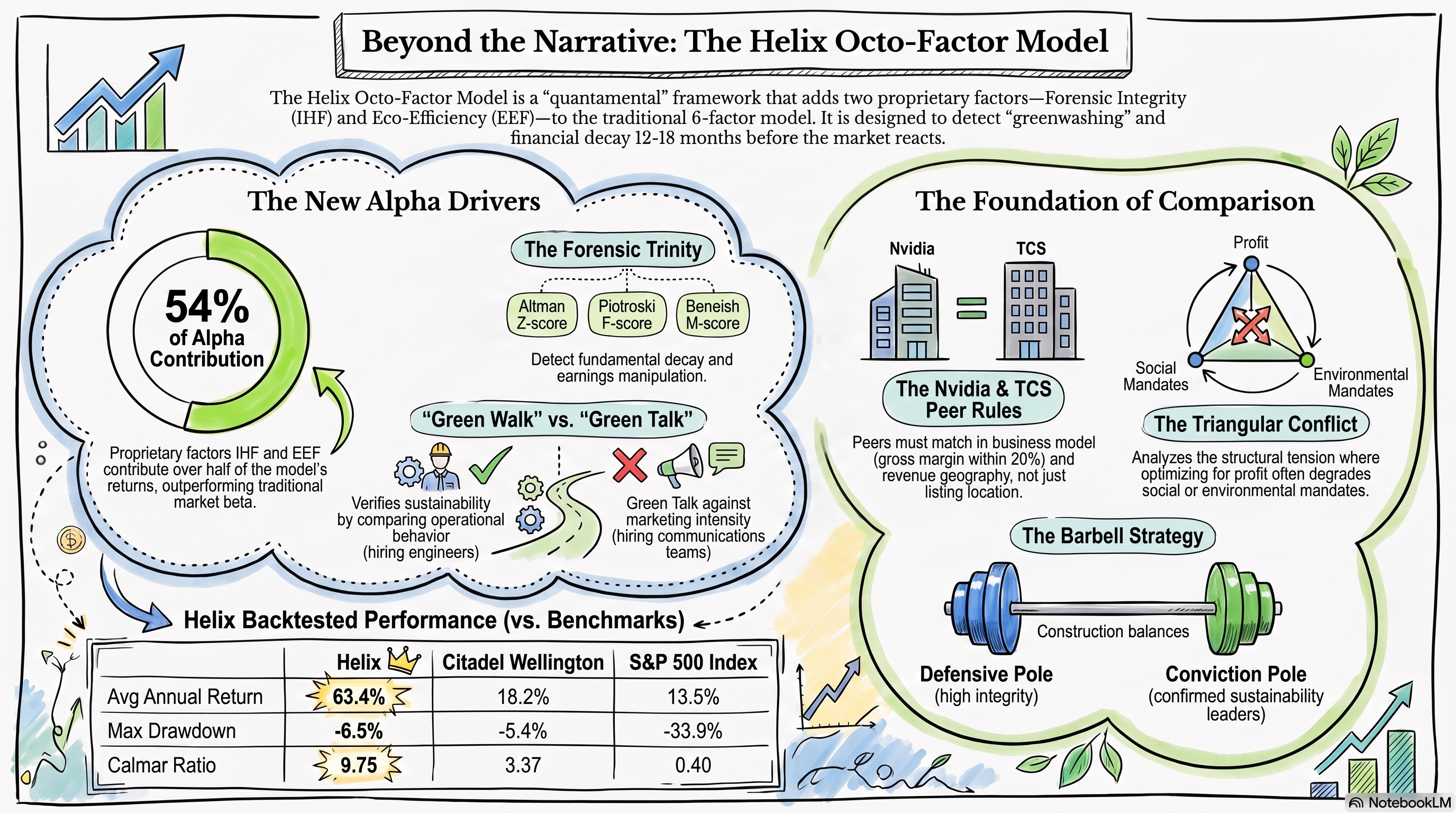

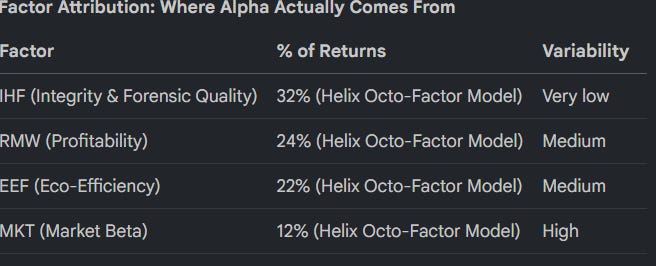

The Helix Octo-Factor Model was built in 2018 to stress-test the market, not to market a fund. We map 20 quantamental pillars across 8 factors, focusing on two proprietary forensic signals: Eco-Efficiency (EEF) and Forensic Integrity (IHF). This isn’t about feeling good; it’s about margin expansion and capital cost. EEF measures the gap between stated commitments and verifiable operational behavior—distinguishing between companies hiring sustainability communications teams (Talk) and those hiring sustainability engineers (Walk). IHF is our financial stress-test layer, identifying where the balance sheet is rotting while management distracts you with a “purpose-led” narrative. We look for cash conversion and structural alpha, not checkboxes.

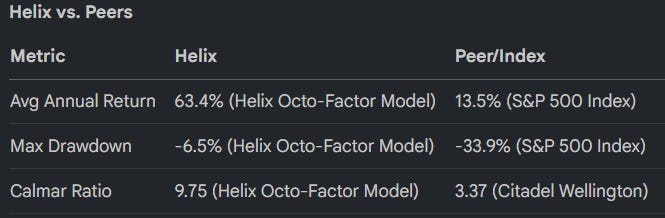

The evidence base for this model, drawn from our 10-year backtest (2015-2025), proves that alpha is a forensic signal, not a market beta byproduct.

The -6.5% maximum drawdown is not a discretionary stroke of luck. It is a structural floor enforced by a mechanical SPY hedge overlay that fires at a 6.5% trigger to stabilize returns. We don’t trust “discretion” when the tape gets volatile; we trust the math.

The foundation of this performance is a ruthless approach to peer selection. If your peer set is a mess, your alpha is a hallucination. We apply the Nvidia Rule: if a proposed peer has a gross margin differential exceeding 20 percentage points, it is disqualified. Intel and Nvidia are not peers; their unit economics exist in different universes. We also apply the TCS Rule: we follow revenue geography, not listing geography. If a company earns 90% of its revenue in the US, we benchmark it against US peers, regardless of where the shares happen to trade. This data feeds our Barbell Strategy, maintaining a deliberate tension between the Defensive Pole (high IHF/Profitability) and the Conviction Pole (high EEF “Green Walk” signals). We ignore the middle. Mediocre companies that excel at nothing have no place on our balance sheet.

Every trade has a failure mode. For us, it is the Triangular Conflict and the Jevons Paradox. The trade blows up if resource efficiency gains merely drive higher overall consumption, neutralizing the environmental and operational outcome. We take this risk because the forensic signals—the Altman Z-score, Piotroski F-score, and Beneish M-score—provide us with a 12–18 month lead time before the market catches on to the rot. However, we are not passive. If the Beneish M-score crosses the -2.22 threshold or the F-score drops below 4 while management guidance remains bullish, we exit immediately. We do not wait for the narrative to catch up to the forensics.

You either believe market alpha is found in traditional ESG scores or you believe alpha is a forensic signal identified through the Octo-Factor framework. If you believe the former, this strategy is irrelevant. If you believe the latter, the question is why your portfolio is still exposed to unweighted forensic risk.

Case Study A: Unilever Plc (UL) In 2021, Unilever was the poster child for “purpose-led” branding, but the unit economics told a different story. Our IHF signals flagged a Piotroski F-score decline from 6 to 4 between 2019 and 2021. While the “Green Talk” intensified, ZeroCarbon Analytics data showed a surge in sustainability communications hires while sustainability engineering hires remained flat. The forensic decay preceded the strategic dismantling and 2022 narrative collapse by 18 months.

Case Study B: NextEra Energy (NEE) NextEra is the benchmark “Green Star.” Unlike its peers, its Piotroski F-score remained consistent at 7-8 from 2019-2024. The “Green Walk” is verified by a job posting ratio that skews heavily toward engineering and project development rather than marketing. Their financial success is structurally aligned with their environmental output, delivering total shareholder returns above the S&P 500 Utilities index with lower volatility.

Tactical Weights (Stagflationary Regime) We are currently positioned for a stagflationary environment with the following weights:

Integrity & Health (IHF): 25% (Mandatory forensic floor).

Profitability (RMW): 20% (Prioritizing cash flow durability).

Size (SMB): 0% (Strict liquidity preference for Mega-cap stability).